Most families in New York get this backwards. They assume a date of death appraisal only matters when the estate is large enough to owe federal estate tax. With the 2026 federal exemption set at $15 million per person under the One Big Beautiful Bill signed in July 2025, almost no estate owes that tax. The appraisal still matters for nearly every heir who inherits a home, and skipping it usually costs far more than the tax ever would.

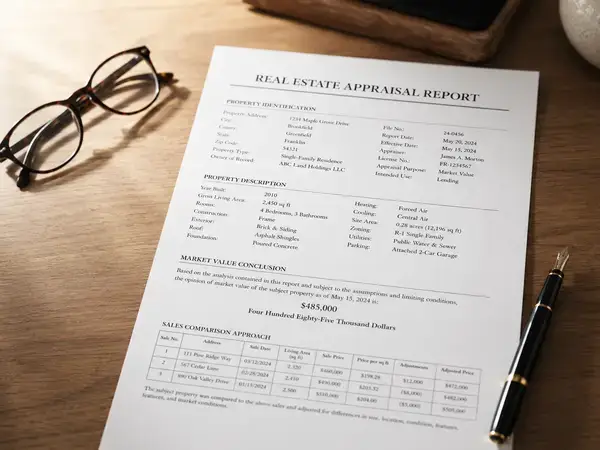

A date of death appraisal sets the fair market value of real property on the exact day its owner died. It supports IRS Form 706, the federal estate tax return, along with probate and dividing assets among heirs. Its biggest job is documenting the stepped-up basis, which decides the capital gains tax heirs pay when they sell.

That last part is where the money sits. It is also the part a generic online estimate cannot handle, because the number has to hold up later, which means it has to come from a New York City appraisal firm that actually works these neighborhoods.

What a date of death appraisal actually does

A date of death appraisal answers one question: what was this property worth on the day the owner died, not today. Appraisers call this a retrospective valuation, because they are looking backward in time.

You will also hear it called a date of death valuation, a probate appraisal, or an estate appraisal. The work is the same. The appraiser pulls comparable sales from around that past date, adjusts for the property’s condition then, and lands on a number they can defend. If you want the finer points of how an appraisal and a valuation differ, the short version is that the words get used loosely, but the method here is formal.

A standard appraisal reflects today’s market. This one rebuilds a past one. That is harder, and it is exactly why the two are not interchangeable.

Worth saying plainly: this is not a Zillow number. It is a USPAP-compliant report signed by a certified appraiser, and that distinction is the whole point.

Appraisers usually rely on the sales comparison approach for homes, bringing in the cost or income approach when the property calls for it. Automated valuation tools keep improving, but on their own they do not hold up for estate or tax work that an examiner might test. The better appraisers treat the retrospective date with extra care, documenting the market exactly as it stood, because a thin analysis is the first thing an examiner picks apart.

Why you need one even when no estate tax is owed

Here is the part most articles skip. Even if the estate owes zero federal estate tax, you almost certainly still need the appraisal, because of the stepped-up basis.

The federal exemption is $15 million per person in 2026, so the vast majority of estates never file Form 706. But the basis rule under Internal Revenue Code section 1014 applies to everyone, no matter how small the estate, and basis sits right at the center of what an executor has to settle.

The risk is quiet and it shows up late. Without a credible date of death value on record, the IRS can question the basis when heirs sell, sometimes years after the death. If you cannot prove the value, you can get taxed on appreciation that happened before the death, plus interest.

I have watched heirs lean on the county assessor’s figure to save a little. The problem is those figures often sit well below market value, and that gap turns into taxable gain the moment the property sells.

The other uses are more familiar: settling the estate, filing the probate inventory, and splitting property fairly among heirs. For a Park Slope townhouse or a Bed-Stuy two-family, none of those numbers are small, which is why bringing in an estate appraiser in NYC early pays off. The same logic drives demand for estate appraisals in Brooklyn, where prices have climbed for the better part of a decade.

There is also the matter of fairness. When several siblings inherit one property, an independent value gives them a shared starting point for a buyout or a split, which heads off the fights that drag estates into court. The same number anchors trust distributions when a home sits inside a trust. In New York, where a single brownstone can be the largest asset in the estate by far, that shared figure is often what keeps a family talking instead of litigating.

What does IRS Form 706 require for real estate?

IRS Form 706 is the federal estate tax return, and it reports every asset in the estate at its fair market value as of the date of death. For real property, that value has to come from a qualified appraisal, not a guess.

The requirements are specific. You need a qualified appraiser with the education and experience to value that type of property. You need a written report that states the effective date, the purpose, a description of the property, the valuation method, and the appraiser’s credentials. You need substantiation, meaning records that back the value, because the IRS can ask for them. And you face penalties if values are misstated.

Qualified here is not a loose word. It means an independent appraiser with real experience in that property type, working at arm’s length from the family and the outcome. An in-house guess or a friend in the business will not carry the same weight if the return is examined.

USPAP is the standard appraisers follow for this work. The instructions for Form 706 lay out how real property gets valued in the gross estate, including the alternative valuation date. For a plain look at what a complete appraisal report includes, the structure carries straight over to estate work.

Two things follow. First, only estates above the $15 million threshold actually have to file Form 706. Second, the ones that do also deal with consistent basis reporting on Form 8971, so the value on the return and the value heirs use later have to line up.

Form 706 vs. Form 709, where families get it wrong

This is the distinction that trips up even some attorneys. Form 706 covers what passes at death. Form 709 covers what you give away while you are alive.

They use different dates. Form 706 values property at fair market value on the date of death. Form 709, the gift tax return, values a gifted property as of the date of the gift instead. The instructions for Form 709 treat an arm’s length sale price near the gift date as the best evidence, with comparable sales as the fallback.

Here is why it matters for real estate, and it runs against common advice. People sometimes think handing the house to their kids before death is the clever move. For appreciated property, it often is not. A lifetime gift carries over the original low basis, with no step-up. Inheriting the same home at death resets the basis to current value. The timing of that transfer can swing the tax bill by six figures.

One nuance to flag: if the donor dies in the same year as the gift, the executor has to file the donor’s Form 709 too. Appraisal firms often handle both, which is why the two forms get blurred together.

There is a quieter reason to get the valuation right on a gift. Adequate disclosure on Form 709, which usually means attaching a qualified appraisal or a detailed write-up of how the value was set, is what starts the clock on the IRS statute of limitations. That point is easy to overlook, because the gift tax rarely comes with a check attached. For most people the lifetime exemption absorbs the gift, so the only real consequence of a sloppy filing is leaving the door open. Skip the disclosure, and the agency can revisit that gift years later.

How stepped-up basis cuts the capital gains tax heirs pay

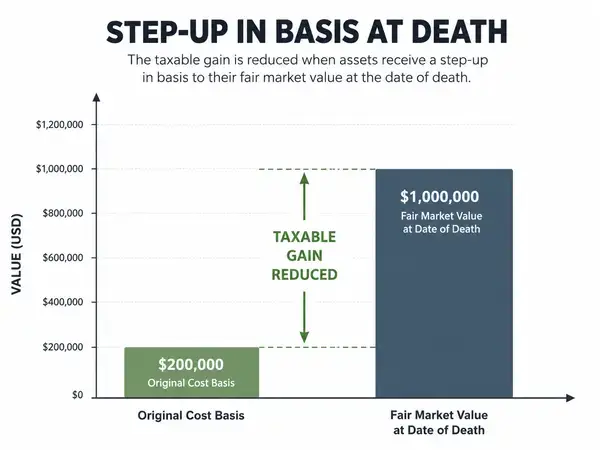

Stepped-up basis is the reason a date of death appraisal pays for itself. When you inherit property, its basis resets to the fair market value on the date of death.

Picture a Brooklyn brownstone a parent bought decades ago for a small fraction of what it is worth today. Without the step-up, an heir who sells owes capital gains on all of that growth. With the step-up, the basis becomes the value at the date of death, so selling near that price leaves little or no taxable gain. The bigger the run-up, the bigger the benefit.

The rates make the stakes plain. Federal long-term capital gains run 15 percent to 23.8 percent once you add the net investment income tax, and New York taxes the gain on top of that. Federal law sets the basis of inherited property at its value on the date of death.

Set the one against the other and the math is lopsided. A retrospective appraisal is a one-time job, and the capital gains tax a clean basis can erase on an appreciated NYC home dwarfs it. That is not a close call.

The appraisal is the proof. No appraisal, no clean basis.

When should you get a date of death appraisal?

As soon as you reasonably can after the death, even though the appraisal can technically be done later.

A retrospective appraisal can be completed months or even years out. It just gets harder. Comparable sales from the exact period get buried, condition details fade, and the work grows. If the property is a home, a co-op, or a small multifamily, line up a residential real estate appraiser in NYC while the records are still easy to pull.

Deadlines push the timing too. Probate has its own schedule, and for a taxable estate, the estate tax return adds pressure. If the estate might use the alternative valuation date, the six-month window needs to be on the radar from day one.

Practical tip from the field: start a folder the same week. Pull the deed, any old appraisals or refinance paperwork, and notes on major renovations and their dates. Old closing statements and prior tax bills help too, especially for a property that has been in the family for decades. Handing that over up front saves the appraiser hours of digging and tightens the final number.

What does FMV mean on a date of death appraisal?

FMV stands for fair market value: the price a willing buyer and a willing seller would agree on, with neither under pressure and both knowing the facts. That is the IRS definition, and it is the number the appraisal targets.

On a date of death appraisal, FMV is that value as of the death date. For homes, appraisers lean on the sales comparison approach, weighing what similar nearby properties sold for around that time. The mechanics of how appraisers reach a value follow the same logic in either case.

The main twist is the date. A home appraisal in NYC done today looks at current comps. This one rewinds the clock to the day the owner died and works from there.

For most homes the comps do the heavy lifting. For an unusual property, a multifamily with rental income or a one-of-a-kind loft, the appraiser may weigh the income or cost approach alongside the sales, then reconcile the three into a single supported value.

The alternative valuation date, and when it actually applies

The alternative valuation date lets an executor value the estate six months after the death instead of on the date of death. It is an option on Form 706, not the default.

The conditions are strict. The IRS only allows it when it lowers both the gross estate and the estate tax. So it only helps a taxable estate whose value dropped during those six months. Any asset sold or distributed before the six-month mark gets valued at that earlier date instead.

A reality check: for almost every estate, the ones under $15 million that owe no federal tax, the alternative valuation date never comes up. It is a tool for the rare taxable estate riding out a market dip, and it needs professional guidance before anyone elects it.

A simple example shows when it helps. If a taxable estate’s main property lost value during those six months, electing the alternative date can lower both the reported estate and the tax due. Outside that narrow case, the date of death value stands.

What drives the cost and timeline of the appraisal

Two things shape what a retrospective appraisal takes: how hard the historical data is to rebuild, and how complex the property is.

Pulling comps as of a past date is more work than grabbing today’s sales, so retrospective reports run heavier than standard ones. NYC adds its own wrinkles. Co-ops, condos with odd layouts, mixed-use buildings, and small multifamily all take more analysis than a single-family out in the suburbs. The number of properties and the depth of the report matter too.

Most reports land in a few weeks. You speed it up by handing over the deed, any prior appraisals, and a record of renovations up front. For a feel of how long the appraisal takes start to finish, it is not far off a standard report, with the research adding time on the front end.

Supply is part of the story too. The Bureau of Labor Statistics counts roughly 62,000 to 77,000 property appraisers nationwide, with employment projected to grow about 4 percent through 2034. Plenty handle routine mortgage jobs, but far fewer do retrospective and estate assignments well, so booking an experienced one early matters in a market as layered as New York.

Now the contrarian part. The cheapest path is usually the costliest. A county assessment, a Zillow estimate, or a realtor’s comparative market analysis is not a USPAP-compliant appraisal, and it will not hold up if the IRS questions the basis down the road. Saving a little now can mean a tax bill later, and by then the cheap number is locked in.

How do you find a qualified appraiser in NYC?

Look for a New York State certified appraiser who follows USPAP and has actually done retrospective and estate work. Those last few words carry the weight.

Work through a short checklist. Confirm the appraiser is certified in New York. Check that they produce a USPAP-compliant report, since the standards come from the Appraisal Foundation. Ask directly about retrospective experience, because rebuilding a past market is its own skill. And confirm the report can serve double duty for probate and for the future capital gains basis, because one good report usually covers both. If you want a fuller rundown on picking the right appraiser, the basics carry over: license, references, and a clear written scope.

A few questions separate a safe hire from a risky one, and most people never ask them. Will the report be USPAP-compliant and defensible if the IRS examines the basis five or ten years from now? How will you handle adjustments for the market and the property’s condition on that exact past date? Can one report serve both probate and the future capital gains basis? Clear answers to those three are a good sign you are in the right hands.

Think of a date of death appraisal less as a tax-season errand and more as a one-time document that locks in a number your family will rely on for years. It sets the basis. It backs up probate. It settles who gets what. Get it done early, by someone who can stand behind the figure, and the rest gets easier. Cut corners, and the bill tends to show up later, with interest attached.

FAQs

Do I need a date of death appraisal if the estate is under the federal exemption?

Yes, in almost every case. The 2026 federal estate tax exemption is high enough that most estates never file Form 706, but the stepped-up basis rule applies no matter the estate’s size. Without a credible date of death appraisal on file, the IRS can question the basis when heirs sell, which can mean tax on years of pre-death appreciation.

Can I use the county assessor’s value or a Zillow estimate instead?

For IRS purposes, no. Assessor values and online estimates are not USPAP-compliant appraisals, and they often sit well below market value. That gap can turn into taxable gain when the property sells, which is why the informal route tends to backfire later.

How does a date of death appraisal affect capital gains tax when I sell?

It sets the stepped-up basis, which is the property’s value on the date of death. Heirs generally owe capital gains only on appreciation after that date. A documented basis can save a large amount when selling an appreciated home, because it removes years of pre-death growth from the taxable gain.

What is the difference between Form 706 and Form 709?

Form 706 is the federal estate tax return, and it values property at fair market value on the date of death. Form 709 is the gift tax return, and it values gifted property as of the date of the gift instead. The two use different valuation dates, and gifting a home during life does not give heirs the step-up that inheriting it does.

Is a date of death appraisal required for probate?

Often yes, depending on the state and the size of the estate. Many courts want an inventory with professional valuations so assets can be distributed and debts settled. A single USPAP-compliant report can usually serve both the probate court and future tax basis documentation.

How long after the death can I still get a date of death appraisal?

It can be done months or even years later, because it is a retrospective valuation tied to the death date. The catch is that historical sales data and condition details get harder to reconstruct over time, so the work takes longer and the value is easier to challenge the longer you wait.

What is the difference between a current appraisal and a date of death appraisal?

A current appraisal reflects today’s market. A date of death appraisal rebuilds the market as of the exact date the owner died, using comparable sales and conditions from that time. The first is for buying, selling, or refinancing. The second is for estate, probate, and tax purposes.