UAD 3.6 is the updated Uniform Appraisal Dataset from Fannie Mae and Freddie Mac that becomes mandatory on November 2, 2026. It replaces the alphabet soup of legacy forms (1004, 1073, 2055, and others) with a single dynamic Uniform Residential Appraisal Report. If you’re buying, selling, or refinancing a home in New York City after that date, your lender’s appraisal will look different, contain more data, and may take a few hours longer to produce. The value of your property won’t change because of UAD 3.6. The paperwork will.

UAD 3.6 is a 2026 data standard from Fannie Mae and Freddie Mac that consolidates legacy appraisal forms into a single dynamic Uniform Residential Appraisal Report. It expands site, view, room, and energy data, delivers reports as structured XML, and becomes mandatory for GSE-backed mortgage appraisals on November 2, 2026.

I’ve watched a handful of these regulatory transitions roll through the appraisal world, and this one is different. The methodology behind value isn’t changing. The reporting format is being rebuilt from the ground up. That distinction matters, and it’s the thing most homeowners get wrong when they hear about it. At Block Appraisals, we’ve been training on the new URAR since the limited production window opened in September 2025. Our certified NYC appraisal team is ready for the mandate.

What Is UAD 3.6 in Plain English?

UAD 3.6 is version 3.6 of the Uniform Appraisal Dataset, the rulebook Fannie Mae and Freddie Mac use to standardize how appraisers report property data. Think of it as the formatting language for mortgage appraisals. Same valuation work. Different report.

The old UAD 2.6 forms were built in an era of fax machines and PDF attachments. They were heavy on free-text narrative and light on structured data. Lenders couldn’t easily pull comparable details across reports, and AI-driven risk tools choked on inconsistent fields.

UAD 3.6 fixes that. The new URAR is a dynamic form. Sections expand or stay hidden based on the property type, the inspection method, and what the appraiser actually finds. It aligns with MISMO v3.6 and delivers as XML to the Uniform Collateral Data Portal so lenders can analyze data instantly instead of paying someone to retype it.

Actually, that framing isn’t quite right. The better way to think about it: the old forms forced every property into the same rigid template. A studio co-op in Chelsea got the same fields as a four-bedroom colonial. The new URAR adapts. That’s the headline.

When Does UAD 3.6 Become Required?

November 2, 2026. After that date, any appraisal submitted to the UCDP for a Fannie Mae or Freddie Mac loan must use UAD 3.6. UAD 2.6 submissions will be rejected.

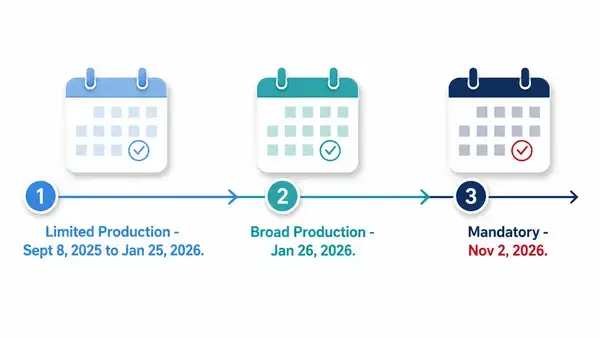

Here’s the full GSE timeline straight from Fannie Mae’s broad production announcement:

1. Limited Production Period: September 8, 2025 to January 25, 2026. Select lenders and appraisers piloting the new format.

2. Broad Production: January 26, 2026. Any lender with compliant software can voluntarily submit UAD 3.6 reports.

3. Mandatory: November 2, 2026. All new appraisals for GSE loans must be UAD 3.6 or they fail submission.

If you’re closing on a New York City home before November 2, 2026, your appraisal may use either standard depending on your lender’s software readiness. After that, it’s UAD 3.6 across the board for any conventional, Fannie, or Freddie-backed loan.

Which Properties Does UAD 3.6 Cover?

UAD 3.6 applies to four residential property types: one-unit detached homes, two-to-four-unit properties, condominium units, and cooperative units. These are the property categories Fannie Mae and Freddie Mac buy mortgages on, which is why their data standard governs the appraisals.

• Single-family houses (one-unit detached, attached, or semi-detached)

• Two-to-four-unit properties (small multifamily that still qualifies for residential financing)

• Condominium units (any project type)

• Cooperative units (a New York staple, finally getting equal treatment in the new form)

It does not apply to mixed-use buildings where the commercial component is significant, true commercial properties, or specialty property types outside the residential umbrella. Those use different forms and reporting standards entirely.

For New York City, the cooperative coverage matters most. Co-ops are roughly half the housing stock in Manhattan, and the old forms treated them awkwardly. If you’re buying a co-op in Greenwich Village or Soho, the appraisal will read cleaner under the new standard. We handle coop appraisals across NYC and the URAR transition is genuinely a step forward for this property type.

How Is UAD 3.6 Different From UAD 2.6?

UAD 3.6 replaces multiple static forms with one dynamic URAR, captures roughly 70+ new structured fields, expands view and site influence options, adds dedicated energy and green feature sections, and delivers reports as machine-readable XML instead of PDF-first narrative.

Here’s the side-by-side:

| What Changed | UAD 2.6 (Current) | UAD 3.6 (New) |

| Form structure | Multiple static forms (1004, 1073, 2055, etc.) | Single dynamic URAR that adapts to property |

| Data style | Free-text narrative dominant | Structured fields with enumerated values |

| View types | Limited categories | 28+ specific view types |

| Site influences | Few options | 20+ site influence types |

| Room ratings | Whole-property ratings | Room-level condition and quality, with +/- modifiers |

| Energy features | Free-text mention | Dedicated section for solar, HVAC, insulation, certifications |

| Delivery format | PDF-focused | XML/ZIP to UCDP for automation |

| Time per report | Baseline | 2 to 4 additional hours reported by appraisers |

The Appraisal Institute calls this a modernization. Most lenders call it efficiency. A lot of working appraisers call it something else, and I think they have a point. We’re trading narrative judgment for structured fields, and there are properties in this city where narrative judgment is the whole job. A turn-of-the-century townhouse in Brooklyn Heights with original details, partial gut renovation, and zoning quirks doesn’t fit into 70 dropdown boxes cleanly. Some of that detail is going to get lost. Pretending otherwise is what gets written into the press releases.

Will UAD 3.6 Change Your Home’s Appraised Value?

No. The methodology for determining market value is unchanged. UAD 3.6 changes the reporting format and data structure, not the analytical work behind the value opinion.

Your appraiser will still inspect the property, pull comparable sales, make adjustments for size and condition and location, and reconcile to a final value. The math is the same. The form looks different. That’s the entire change.

This is the single biggest piece of misinformation circulating right now. I’ve fielded calls from sellers worried that the new forms will somehow lower their value, and from buyers convinced appraisals will get stricter. Both are wrong. The standard tells appraisers how to report data. It doesn’t tell them what numbers to put in.

Will My Appraisal Take Longer Under UAD 3.6?

Yes, at least during the transition window. Working appraisers report the new URAR adds roughly 2 to 4 hours of work per report compared to the legacy forms. Expect that to translate into longer turn times through the first half of the rollout.

The extra time comes from the new structured fields. Room-level condition and quality ratings, expanded view and site influence enumerations, dedicated energy and green sections. None of these existed in UAD 2.6, so the appraiser has to gather and document more on-site, then map it correctly into the digital form.

Whether that adds to your final invoice depends on the firm. Some shops will absorb the extra time into existing fees because they’ve already eaten the software and training costs as a business expense. Others will pass through a portion. Ask before you book. And if a firm dodges the question or gives you a non-answer, that tells you something about whether they’ve actually prepared for the mandate or are about to scramble through it in October.

For complex NYC properties (prewar co-ops, irregular townhouses, mixed-use that still falls inside the residential umbrella), expect the longer end of that 2 to 4 hour range. Simpler one-unit suburban-style homes in Staten Island or Eastern Queens will land closer to the lower end.

Does UAD 3.6 Apply to Non-Mortgage Appraisals?

No. UAD 3.6 only governs appraisals ordered by mortgage lenders for GSE-backed loans. Estate, divorce, tax appeal, litigation, and pre-listing appraisals are not affected.

This is the cleanest line in the whole standard. If your appraisal is going to Fannie Mae or Freddie Mac via a lender, UAD 3.6 applies. If your appraisal is going to a probate court, a divorce attorney, an IRS auditor, a tax assessor, or your own kitchen table, it doesn’t.

Non-lending appraisals follow USPAP, the Uniform Standards of Professional Appraisal Practice, which sets the ethical and methodological floor for every licensed appraiser in the country. USPAP doesn’t care what form you fill out. It cares whether your analysis is defensible. So our estate appraisals in Brooklyn, divorce appraisals, and litigation work will look the same on November 3, 2026 as they did the day before.

What Should NYC Homeowners Do Before the Mandate?

If you have a mortgage appraisal coming up in 2026, ask your appraiser two questions: which version of UAD they’re submitting under, and what software platform they’re using. Both answers should come easily. Hesitation is a flag.

Practical preparation for your UAD 3.6 appraisal:

4. Document any energy-efficient upgrades. The new form has dedicated structured fields for solar, high-efficiency HVAC, insulation upgrades, and green certifications. Have records ready.

5. Allow access to every room. Room-level ratings are now standard. Locked doors and inaccessible spaces will trigger revision requests under the new format.

6. List recent improvements with dates and costs. Kitchen and bath renovations, roof replacement, HVAC, window upgrades. Specifics help.

7. For co-ops and condos, have your board package, building financials, and any flip tax information available.

8. Ask if your lender’s software is UAD 3.6 ready. Some smaller lenders are still catching up.

And ask the question almost no one asks: what’s the appraiser’s revision protocol under the new structured format? Reports will get kicked back for missing enumerated fields more often during the transition. You want a firm that has thought through this. An appraiser who has lived inside the new URAR for a year will outperform one who is reading the field guide in the parking lot before your inspection. Preparation shows.

What Are the Biggest Risks During the Transition?

The biggest risks are software bugs, longer turn times, and rejected submissions. Early adopters are reporting issues with sketch tools, fields that don’t populate correctly, and inconsistent interpretation of the new enumerated values.

According to BLS occupational data on appraisers, there were 77,300 property appraisers and assessors in the U.S. as of 2024, with projected employment growth of 4% through 2034. That sounds healthy. The wrinkle: a meaningful share of older appraisers (35 to 50 years of experience) are choosing to retire rather than invest in UAD 3.6 software and training. The labor pool is shifting under the new standard, and turn times will reflect that for at least the first six months after the mandate.

For NYC specifically, the higher-than-average property complexity means the new form will run longer here than in simpler markets. A standard suburban appraisal in the Midwest might add an hour. A Manhattan co-op with prewar quirks and a corner-lot influence will easily run three to four hours longer than under the old format.

How Does UAD 3.6 Treat Energy and Green Features?

UAD 3.6 introduces dedicated structured fields for energy-efficient and green features, including solar systems, high-efficiency HVAC, insulation upgrades, and third-party certifications. The fields make these features visible to lenders for the first time, but they don’t automatically add value to the appraisal.

This is the most misunderstood new feature in the form. Homeowners hear ‘dedicated green section’ and assume their solar panels will finally get credited. Not exactly. The appraiser still has to find comparable sales that demonstrate market reaction to those features. If similar homes in your area are selling for a premium because of solar, the comp adjustments reflect that. If they’re not, the green fields are documentation only.

Where this matters most: marketability and obsolescence analysis. A high-end Brooklyn townhouse with a Passive House certification reads differently to a lender when those features are in structured fields versus buried in narrative. Whether that translates to value depends on the comps.

Closing Thought

UAD 3.6 is the biggest formatting overhaul to mortgage appraisals in a generation, and it lands as a hard mandate on November 2, 2026. The new URAR captures more data, delivers cleaner files, and forces every appraiser in the country to retool. What it doesn’t do is change how your property is valued. If you’re buying, selling, or refinancing in New York City, the practical move is to work with an appraisal firm that already runs UAD 3.6 ready software and has trained appraisers on the new fields. Block Appraisals has been preparing for this transition since the limited production window opened, and we’re delivering compliant reports across Brooklyn, Manhattan, and the boroughs today. Reach out through our residential appraisal services in Brooklyn or our mortgage appraisal page to start a conversation about your property and what UAD 3.6 means for you.

FAQs

Will UAD 3.6 change my home’s appraised value?

No. UAD 3.6 changes the reporting format, not the valuation methodology. Appraisers still inspect the property, pull comparable sales, and develop a value opinion the same way. The final number is unaffected by the form change. This is one of the most common misconceptions about the November 2, 2026 mandate.

Will my appraisal cost more under UAD 3.6?

There is no mandated fee increase tied to UAD 3.6. Whether your individual appraisal costs more depends on the firm. Some absorb the additional time required by the new format. Others may pass through a portion. Ask your appraiser directly before scheduling. National average appraisal pricing is set by market factors, not by the data standard itself.

When does UAD 3.6 become mandatory?

November 2, 2026. After that date, all appraisals submitted to the Uniform Collateral Data Portal for Fannie Mae and Freddie Mac loans must use UAD 3.6. UAD 2.6 submissions will be rejected. Limited production began September 8, 2025 and broad production opened January 26, 2026.

Does UAD 3.6 apply to all appraisals or only mortgages?

Only mortgage appraisals for GSE-backed loans. Estate, divorce, tax appeal, litigation, and pre-listing appraisals are not affected by UAD 3.6. Those continue under USPAP, the broader professional standards that apply to all licensed appraisers regardless of the report’s purpose.

What properties are covered by UAD 3.6?

Four residential property types: single-family one-unit homes, two-to-four-unit properties, condominium units, and cooperative units. Mixed-use buildings, commercial properties, and specialty property types fall outside the standard and use different reporting forms.

How long will a UAD 3.6 appraisal take?

Initial transition reports are running 2 to 4 hours longer than the equivalent UAD 2.6 reports. Turn times will likely lengthen across the industry through early 2027 as appraisers, software platforms, and lenders work out friction in the new format. Complex NYC properties will see longer delays than simpler markets.

Will energy-efficient features finally get credit in my appraisal under UAD 3.6?

The new URAR has dedicated structured fields for solar, high-efficiency HVAC, insulation, and green certifications. Whether those features add value still depends on whether comparable sales show buyers paying a premium for them. The form makes the features visible. The market decides if they’re worth money.