A gift tax appraisal is a dated, written opinion of what a property is worth, used to back up the value you report to the IRS when real estate changes hands by gift or at death. It puts a defensible number on the return, and that number decides whether tax is owed, how much, and what your heirs owe later.

One clarification, since the title bundles two things that aren’t identical. Form 709 is the federal gift tax return, filed while you’re alive. Property passing at death goes on Form 706, the estate return. Same core need: a fair market value the IRS will accept, the kind an estate appraisal provides.

A gift tax appraisal is a qualified, date-specific opinion of a property’s fair market value, prepared to support the amount reported when real estate is gifted on Form 709 or passed at death on Form 706. It fixes the value the IRS measures your transfer against and protects you if that value is later challenged.

What a Gift Tax Appraisal Actually Does

A gift tax appraisal does one job: it proves the number.

It backs up fair market value so the figure on your return holds up. On a gift return, a qualified appraisal supports what the IRS calls adequate disclosure, which starts the three-year window the agency has to challenge the value. Skip it and that window may never open. For estates, the Form 706 instructions say to explain each value on Schedule A and attach the appraisals.

There’s a second job most people miss. The appraisal also sets the cost basis the heirs use when they sell. That’s where the bigger stakes usually sit, more on that below.

What separates a report that survives an audit from one that doesn’t:

1. A value tied to a specific date, the date of death or the date of the gift.

2. Real comparable sales with the adjustments shown, not an automated guess.

3. The appraiser’s credentials and a USPAP-compliant method.

4. Enough detail that a reviewer can follow the logic without a phone call.

Form 706 and Form 709 Are Not the Same Form

Form 706 covers estates. Form 709 covers gifts. The valuation logic carries across both, but the date changes.

For an estate, value is set as of the date of death, or an alternate date six months later if it lowers the tax. For a gift reported on Form 709, value is set the day you hand it over. Same property, two snapshots, two numbers.

| Form 706 (Estate) | Form 709 (Gift) | |

| What it reports | Real estate passing at death | Real estate given during life |

| Who files | Executor or trustee | The person making the gift |

| Valuation date | Date of death (or 6-month alternate) | Date of the gift |

| Appraisal step | Schedule A: attach the appraisal | Backs up adequate disclosure |

| Filing deadline | 9 months after death (6-month extension via Form 4768) | April 15 of the following year |

That date matters more than people expect. A Park Slope brownstone’s value can shift sharply across one spring market. The date your appraiser locks in is the date the IRS holds you to.

Who Has to File Form 706 in 2026?

Almost nobody, at the federal level. For 2026, an estate files Form 706 only if it tops $15 million, plus any large lifetime gifts already made.

That figure is new. The One Big Beautiful Bill Act, signed in July 2025, made the higher exemption permanent, up from $13.99 million the year before. Couples can shield $30 million combined. Anything over the line is taxed at up to 40%.

Only estates above that line file at all. Out of roughly 3 million US deaths a year, only a few thousand send in a 706. So most families are clear of federal estate tax. But the federal line isn’t the only one that matters, and the other sits much lower.

When the Appraisal Is Due, and Why Waiting Hurts

The 706 is due nine months after the date of death. You can ask for a six-month extension with Form 4768, but that extends the filing, not always the payment.

The appraisal has to reflect value as of the date of death, not the day the appraiser arrives. The longer you wait, the harder it gets to rebuild what the property was worth months back. Comparable sales fade. Condition notes get fuzzy.

I’ve watched executors sit on this for a year, then scramble. The data is usually still there, but it takes more digging and the number is easier to second-guess. Order it early.

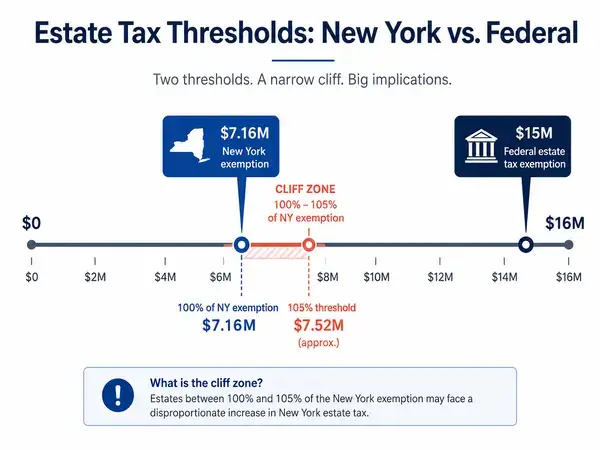

Why NYC Estates Get Caught When the Rest of the Country Doesn’t

New York taxes estates at a far lower threshold than the federal line, less than half of it. And it punishes going even a little over.

The state uses a cliff. If your taxable estate lands more than 5% above the exemption, you lose the exemption entirely and the whole estate is taxed, not just the part over the line. The rate climbs to 16%. New York also doesn’t allow portability between spouses, so a survivor can’t pick up the unused half.

NYC property is expensive enough that this catches regular families, not just the very rich. One Brooklyn Heights brownstone can be worth more than New York’s entire exemption on its own. Add a co-op on the Upper West Side and a brokerage account, and an estate that owes nothing federally can still owe New York a serious bill.

So the appraised value does real work here. The gap between sitting just under New York’s line and just over it isn’t rounding. It’s the difference between owing nothing and owing the state a large bill, which is why the date and the number have to be right.

Can You Use an Online Estimate or the Assessor’s Value for the IRS?

You can try. It’s a bad idea for anything the IRS might look at closely.

Online value estimates run on public data and broad models. They don’t know that a Tribeca condo had its kitchen gutted last year, or that a unit faces a brick wall instead of the park. County assessed values are built for property tax, not federal transfer tax, and often trail the market by years. People assume a government number is one the IRS will take. It’s backwards: the assessor and the IRS measure different things.

If the IRS disagrees, it can reassess. That can mean more tax, interest, and accuracy penalties that run 20% to 40% of the underpayment on a serious misstatement. A qualified appraisal usually settles it before it gets that far.

The Step-Up in Basis Most Families Miss

This is where most families lose the most. When you inherit property, its tax basis resets to fair market value at the date of death. That reset is the step-up.

Basis is what you subtract from the sale price to find the taxable gain. Higher basis, smaller gain, smaller tax when it sells. Say your mother bought a Harlem townhouse decades ago for a small fraction of what it’s worth today. An appraisal documenting its date-of-death value resets the basis to that figure and can erase almost all the gain her heirs would otherwise be taxed on.

Now the mistake I see in the name of smart planning. People gift the appreciated property to their kids while alive, sure they’re doing a favor. But gifts don’t get the step-up. The kids take the old, low basis and carry the built-in gain with them. When they sell, they can owe capital gains on decades of appreciation a step-up would have wiped out. Under today’s high exemption, most of these families were never going to owe estate tax anyway. They trade a tax they’d never pay for one they will.

That’s the question almost nobody asks an advisor: how does this transfer hit my heirs’ capital gains, not just my estate tax? Get the valuation right and the step-up on record, because the IRS now wants the heirs’ basis to match the value on the estate return.

Do You Always Need a Formal Appraisal?

No. And anyone who says to always get one, just in case, is usually selling appraisals.

If an estate sits well under both the federal and New York lines and nobody plans to sell soon, a full qualified report for the IRS can be overkill. I’d rather say that than sell you something you don’t need.

But the moment any of these is true, get the real thing: the estate is near New York’s exemption line, the property is unusual or hard to compare, it’s held in an LLC or trust, or someone will sell within a few years and wants the step-up documented.

One warning. USPAP-compliant on a website doesn’t promise a report that holds up. Plenty of appraisers do fine mortgage work but rarely touch date-of-death or gift valuations, which follow their own rules. Look for a certified appraiser who does estate and tax work often and can show it.

A gift tax appraisal does more than satisfy a filing. It sets the number the IRS taxes against, the basis your heirs inherit, and the figure that drives their capital gains years out. Set it on the right date, get it from a licensed NYC appraiser who handles estate and gift work often, and order it before the trail goes cold. With this much tax riding on a single number, it’s not a figure to guess at.

FAQs

Do I need a formal appraisal to gift real estate to my family?

Not for small gifts, but it’s strongly advised once a gift to one person passes the annual gift tax exclusion and triggers a Form 709 filing. A qualified appraisal supports the value you report and starts the clock on the window the IRS has to challenge it. County assessor values are risky for this.

What is the difference between a gift tax appraisal and an estate tax appraisal?

Both put a defensible fair market value on real estate, but the valuation date differs. A gift tax appraisal values the property as of the date of the gift for Form 709. An estate appraisal values it as of the date of death, or an alternate date six months later, for Form 706. Same method, different snapshot.

Can I use an online estimate or my county assessor’s value for IRS gift or estate tax reporting?

You can, but it’s risky for anything the IRS examines closely. Automated estimates and tax-assessed values aren’t built for federal transfer tax and often miss condition, renovations, or local detail. If the IRS revalues the property, accuracy penalties can run 20% to 40% of the underpayment on a serious misstatement. A qualified appraisal is the safer record.

If my estate is under the federal exemption, do I still need a real estate appraisal?

Often yes, even though no federal estate tax is due. The federal exemption is high enough that most estates owe nothing federally, but New York taxes estates at a much lower threshold, so many NYC estates still file at the state level. An appraisal also sets the stepped-up basis your heirs rely on when they sell, which can reduce the capital gains tax they owe later.

How long do I have to file Form 706 after a death?

Form 706 is due nine months after the date of death. You can request a six-month extension with Form 4768, though that extends the filing, not necessarily the payment. The appraisal should reflect value as of the date of death, so it’s best to order it early while comparable sales are easy to document.

What is a gift tax appraisal used for?

A gift tax appraisal is used to prove the fair market value of real estate transferred by gift or at death, so the figure on Form 709 or Form 706 holds up with the IRS. It fixes the value your transfer is measured against, supports adequate disclosure, and documents the basis that decides your heirs’ future capital gains.